In the current lending landscape, efficiency is everything. Traditional appraisals can create delays that slow down loan processing and impact borrower experience. As lenders push to streamline workflows and shorten turn times, hybrid appraisals are emerging as a practical solution to meet growing expectations without compromising valuation quality.

Hybrid appraisals divide the valuation process. A trained third-party, commonly an inspector, collects detailed interior and exterior property data, which a licensed appraiser then uses to complete the appraisal remotely. This method accelerates turnaround times while maintaining appraisal quality. Reports are completed using standardized forms: Form 1004 Hybrid for single-family homes and Form 1073 Hybrid for condominiums.

Fannie Mae implemented hybrid appraisals into its Selling Guide on February 5, 2025, with Desktop Underwriter updates effective March 22, 2025. Freddie Mac followed, making hybrid appraisals available through its Loan Product Advisor as of April 7, 2025. These updates expand eligibility to include purchases and refinances for one-unit properties, such as single-family homes, condos, and PUDs, across primary, secondary, and investment use cases. This marks a significant step in appraisal modernization, offering lenders a faster, scalable alternative to traditional appraisals.

Hybrid appraisals offer several key advantages over traditional valuation methods:

These benefits make hybrid appraisals a compelling option for lenders aiming to enhance efficiency and reduce costs in the appraisal process.

While hybrid appraisals open the door to faster, more efficient valuations, they aren’t a one-size-fits-all solution. Fannie Mae and Freddie Mac have clearly defined where these appraisals can and can’t be used.

Hybrid appraisals are approved for a wide range of residential properties, including:

Certain property types fall outside the current scope, including:

Lenders must assess eligibility early in the loan process to determine if a hybrid appraisal is a fit. While hybrids offer speed and cost advantages, traditional appraisals are still required for more complex or higher-risk properties.

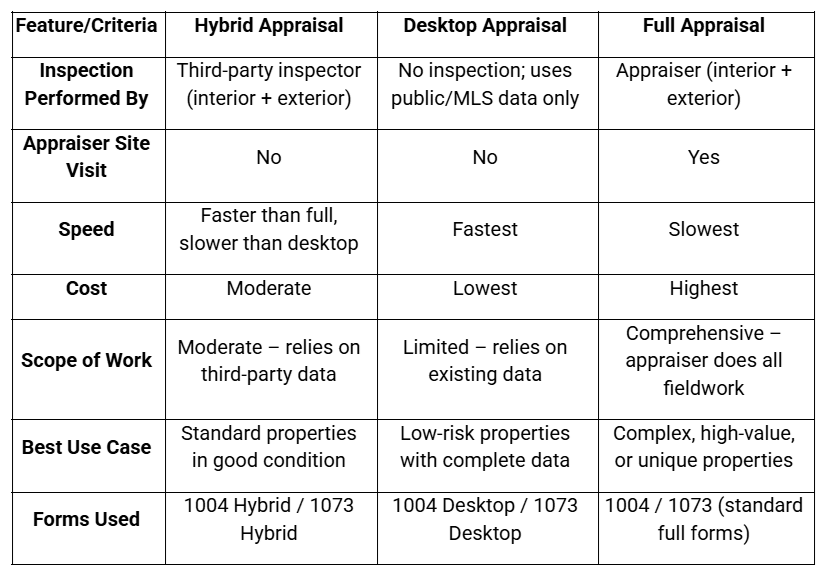

Here’s a quick comparison to help you understand how Hybrid, Desktop, and Full Appraisals stack up against each other:

This breakdown helps determine which appraisal type best suits the loan scenario, balancing speed, accuracy, and compliance.

Despite their advantages, hybrid appraisals come with important considerations. Appraisers may hesitate due to liability concerns – relying on third-party data requires confidence in its accuracy. Data reliability is critical, and inconsistencies can trigger a shift to full appraisals. Additionally, adoption is gradual; some lenders and appraisers are still adjusting workflows and gaining familiarity with the model. Clear guidelines, robust data collection standards, and industry education will be key to successful, widespread hybrid appraisal adoption.

ValueLink makes it easy to adopt hybrid appraisals with full support for 1004 and 1073 Hybrid forms, integrated data collection, and seamless appraiser collaboration. Book a free consultation with our experts to explore how hybrid appraisals can streamline your workflow, reduce costs, and improve turnaround times

👉 sales@valuelinksoftware.com

© 2025 ValueLink and all related designs and logos are trademarks of ValueLink Software, a division of Spur Global Ventures Inc.